The storyline wasn’t

supposed to go like this. As the real

estate market crawled out of its darkest hour, there were going to be plenty of

hurdles; rising interest rates, unemployment, tightening lending standards, and

even over caution. But even the most

pessimistic analysts never expected one particular obstacle to stand in the way

to rosier days for the housing market; a shortage of inventory.

How low are inventory levels?

There are plenty of

statistics to present for your consideration but the most obvious is this;

residential housing inventory levels are currently about 50% lower than normal

and only about 35% of what they were at the peak of the real estate book in

2007. Even in California’s

The number of days a home

sat on the market last month jumped to 72 from 56, causing some concerns of a

potential cool off. The National Association of Realtor’s last quarterly

report cited that housing inventory fell 9.3% at the end of December, to 1.86

million available homes. That equates to

a 4.6-month supply at the current sales pace, where a normalized market yields

about 6 to 7 months of supply.

The number of days a home

sat on the market last month jumped to 72 from 56, causing some concerns of a

potential cool off. The National Association of Realtor’s last quarterly

report cited that housing inventory fell 9.3% at the end of December, to 1.86

million available homes. That equates to

a 4.6-month supply at the current sales pace, where a normalized market yields

about 6 to 7 months of supply.

But the inventory shortage

goes deeper, affecting the low end of the market where first-time buyers and

affordable housing for working families is most prevalent. If you take out investors, cash buyers, and

the high-end market of home sales, we’re faced with a particular dirge of

inventory.

Why we thought inventory would be higher:

As we stated before,

interest rates are still low, banks are eager to lend again, employment and

wages are stable if not optimistic, and buyer demand is there. In some markets, home sales and appreciation

are hot, once again, so it was reasonable to assume sellers would put For Sale

signs in their yards to cash in. The

prevailing theory was that there would be a surplus of inventory for buyers, as

so many foreclosures and short sales hit the market for home shopper to choose

from.

The 4 factors why inventory is so low:

1. Underwater

homeowners.

There’s a significant

segment of homeowners who may want to sell but can’t. It’s reported that currently, 18.8 percent of

homeowners are in a negative equity position, or underwater on their

homes. That’s a vast improvement from

31.4 percent in 2012, but still high.

Just as importantly, 36.9 percent of homeowners are “effectively

underwater,” in their properties, meaning they don’t have enough positive

equity to sell or sell and make any profit.

Add it up and you get more than 18 million homeowners who are forced to

sit on their homes even when they might prefer to move or move up. That’s a huge number of potential inventory

stuck on the shelf.

2. New

construction is lagging.

During the real estate boom,

homebuilders threw up new projects at a record pace, many of them in the modest

price range to attract first time buyers and starter homes for the average

family. But once the balloon popped, they

stopped building and sat on the sidelines to wait for the recovery. This did a couple things – it forced the

small homebuilders, estimated at 50 percent of the market – out of business. It also made them readjust their strategy

when they went back to work, focusing more on larger and luxury homes to build,

not the lower end, to hedge their bets this time.

New home inventory saw the

bottom in 2012 and has edged upward, though still at a 40-year low - only about

800,000 new home starts compared to 1.5 million in a normal market. But again, many of these are multifamily

units to cash in on rental demand or higher-end projects. Now, previously owned homes are selling more

than 10-to-1 to new homes, which accounted for a larger section of inventory

than in the past.

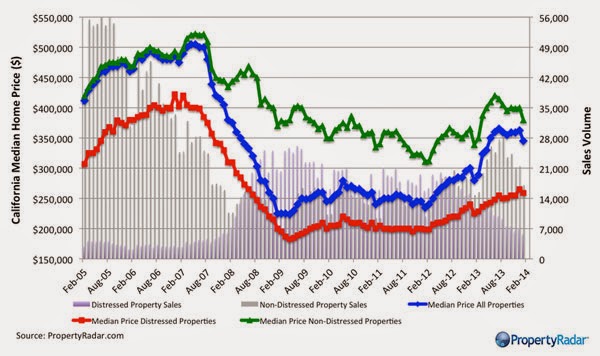

3. Distressed

homes have slowed.

With a flood of foreclosures

and short sales turning over in the recent past, we expected a much larger

inventory for buyers to choose from.

They did account for a large portion of the inventory on the bottom of

the market for buyers to sift through, with over 1 million lender-owned sales

in 2010. But since then, the release of foreclosures has slowed to a crawl. In

fact, at the point of the most current big housing reports, foreclosure starts

had declined at least 22 consecutive months.

Foreclosure activity is still two to three times higher than normal but

still is at its lowest since 2006, about 50 percent less than 2010 short sales

and foreclosure sales accounted for 18.5% of sales in 2013 but only 14.5% of

sales in the first quarter of 2014. A

larger portion of these are taking place in higher end home prices.

4. Consumer

caution.

Consumer confidence drives

markets. When the masses understand there is money to be made, or opportunities

to be had, it opens the floodgates on home buying and selling. Prices go up and that feeds more consumer

confidence. But this time it’s

different. Most vital economic

indicators may be pointing to the fact that it’s a good time to sell your home

to cash in, but in general there’s a blanket of caution draped over the

market. People are just hesitant to make

the wrong move or get on the roller coaster we saw as boom went to bust in the

recent past. They also may not be at the

tipping point yet where they believe the benefit of selling their home will

outweigh risk of the unknown or having to become a buyer in the same market

they sell in. That’s not necessarily a

bad thing, but hesitancy for its own sake doesn’t help people make wise

financial moves. We’re not quite at the

“paralysis-by-analysis” stage, but homeowners are just looking for more

information.

How about in California?

Of course, California is its

own animal, with the highest highs (and the lowest lows.) We’ve seen robust appreciation in many

markets in the Golden State, and the good news is that inventory, though still

being outpaced, is slowly keeping up. In

Los Angeles, inventory is up 17.8 percent year-over-year. San Diego is up

18.6 percent, and our own Sacramento area is enjoying a 23.9 percent gain in

inventory. That’s great news, though

California inventory levels are still 18% lower than normal and 2014’s first

quarter sales numbers have been weaker than expected.

What will solve this paradox?

Time. Tight inventory leads to price appreciation, which

entices seller to sell to cash in and also spurs the interest of buyers, keeps

interest rates favorable, incentivizes lenders to lend, and signals that all

factors are whistling “all aboard,” for housing. Appreciation will also lead to less underwater

homes and more sellers. Even though

appreciation numbers may be a little cooler than originally anticipated,

“stabilization,” is the name of the game, which will sooth consumer hesitancy. Banks will also continue to release

distressed properties from their books, and new homebuilders will see risk in

entry-level and modest projects.

As cliché as it may sound,

time (perhaps a healthy summer of activity?) should normalize the market’s

inventory levels. In fact, NAR’s April report for existing home sales showed

the first positive news in a long time, an increase in home inventory from a

5.1-month supply to a 5.9-month supply, fantastic news for a real estate trying

to untangle its inventory paradox.

Overstock Buyers - National Wholesale Overstock, Inventory Liquidator, We Buy and Sell Toys, Housewares, Gifts, Home Decor, Novelties, School Supplies, Juvenile Products, Party Goods and Furniture

ReplyDelete